The importance of revitalising the tourism industry’s digitalisation

The sectors most closely related to tourism are digitalising faster than the average for the Spanish economy but there is still a long way to go, especially when compared to other tourism industries in Europe. In the next few years, it will be crucial for Spain’s tourism industry to be able to remedy this situation by means of a clear commitment to digitalisation, which will help to improve its long-term growth capacity. The European NGEU funds are an opportunity to revitalise investment in the digitalisation of tourism businesses after two very tough years for the industry.

Digitalisation has gained even more prominence in our lives In the wake of the pandemic. Consumers have radically changed how they communicate, work and consume and the business fabric has adapted very quickly to these changes, accelerating its digitalisation with the extensive implementation of teleworking and enormous growth in e-commerce sales.14 This transformation is crucial to ensure the long-term growth of all sectors. Companies that invest in digitalisation in the coming years will be investing in a strategy that will help them to gain in productivity and competitiveness and will therefore improve their prospects considerably, while those that lag behind may lose prominence.

Some sectors, such as retail, have made great strides during the pandemic thanks to the unprecedented incorporation of digitalisation into their sales channels. The tourism industry has also realised the importance of e-commerce although, due to the economic problems it has experienced during the pandemic, it has not been able to make such remarkable progress. Nevertheless, the industry’s economic recovery and the arrival of the Next Generation EU (NGEU) funds could provide an impetus for the sector to continue digitalising.

- 14. See «e-commerce: years of progress in just a few months» from our Retail Sector Report 2021 and the Focus «The COVID-19 outbreak boosts remote working» from our June 2020 Monthly Report.

To understand the next steps that should be taken by the tourism industry in digitalisation terms, we need to understand the current state of the businesses in the sector. We have used the CaixaBank Sectoral Digitalisation Index (CSDI) to gauge the extent of digitalisation in tourism companies. Our index provides a holistic view of the business digitalisation process, identifying the strengths and weaknesses of the different sectors of activity in various areas: digital assets (capital and human resources); digital intensity of interactions with clients, suppliers and public authorities, and how intensively both traditional and emerging digital technologies are used.15

As can be seen below, according to the CSDI for 2020 the benchmark sector in Spain is information and communications technology (ICT) with a score of 67 points out of 100.16 Retail, accommodation and transport and storage (the three sectors most closely linked to tourism that are covered by the index) scored 48, 46 and 42 points, respectively, which implies a significant gap with respect to more digital sectors. It should be noted that, although there is no significant difference in any of these three sectors most closely linked to tourism, the trend between 2017 (the first year calculated) and 2020 has been more positive than average, suggesting that the tourism industry is improving its relative position.

CaixaBank Sectoral Digitalisation Index (CSDI)

Index between 0 (min.) and 100 (max.)

the tourism sector is digitalising faster than the average for the Spanish economy

The CSDI enables us to carry out a more in-depth analysis as it is composed of various pillars and sub-pillars that illustrate the degree of digitalisation in more specific fields. In this respect, if we analyse the digitalisation pillars for inputs and interactions (see the table), it can be observed that businesses in the tourism industry stand out in particular areas. We can see that the accommodation sector stands out in digitalisation terms regarding its client relations, thanks to the marketing of services being digitalised, a process that has been gaining ground over other traditional marketing methods for many years now. On the other hand, it is evident that many areas still need improvement, such as the digitalisation of supplier relations and banking, as well as the digitalisation of the factors of production (capital and labour).

Breakdown of the CSDI 2020 by component of the input pillar and interaction pillar

Index between 0 (min.) and 100 (max.)

This analysis raises the question of to what extent it is necessary for the digitalisation of the tourism industry to advance to the same extent as a sector such as ICT. Due to the idiosyncratic features of each sector, the optimal extent of capital and labour digitalisation may vary greatly between sectors. To better understand the gap with the technological frontier of each tourism-related sector, we analysed the degree of digitalisation of the factors of production at an international level, specifically by comparing the degree that advanced digital technologies are used in EU countries for the accommodation and retail sectors.

As can be seen in the following charts, the use of big data and cloud computing technologies by Spain’s accommodation and retail sectors is below the EU average. Moreover, there is a very wide gap between them and the technological frontier (the difference with respect to the most digitalised European country) in all cases, indicating the great room for improvement in tourism-related companies in Spain.

Companies using digital technologies in the EU-27 countries

% of total for each country

of its client relations, thanks to the digitalisation of its marketing services

Having analysed the strengths and weaknesses of the digitalisation process in the tourism industry, it is important to determine what this process can offer companies since digitalisation is not an end in itself but a means of increasing competitiveness and productivity. In this respect, the tourism sector can learn from what the industry itself has gained from digitalising its interactions with clients, a process which, according to the CSDI, has reached a very high level, mainly as a result of the emergence of OTAs (online travel agencies, such as Booking and Expedia) and the development of direct online sales by the major hotel chains.

According to a Phocuswright study, between 2014 and 2019 turnover from hotel room sales in the EU made via electronic channels were very strong, growing at an average annual rate of 8.1%, especially through OTAs whose sales increased by 11% per year. This contrasts with the poorer performance of traditional sales channels (direct face-to-face, physical travel agencies and tour operators), which barely grew at an annual rate of 0.8%. Consequently, the relative share of online sales in the EU reached 40% in 2019 (27% OTAs and 13% direct online sales), suggesting that these sales channels are much more competitive than traditional ones in the eyes of tourists. These trends become even more evident when we look specifically at hotel SMEs, which between 2016 and 2019 only recorded growth in sales channels that were not face-to-face.

grew at an average annual rate of 8.1%, much higher than the 0.8% posted by sales via traditional channels

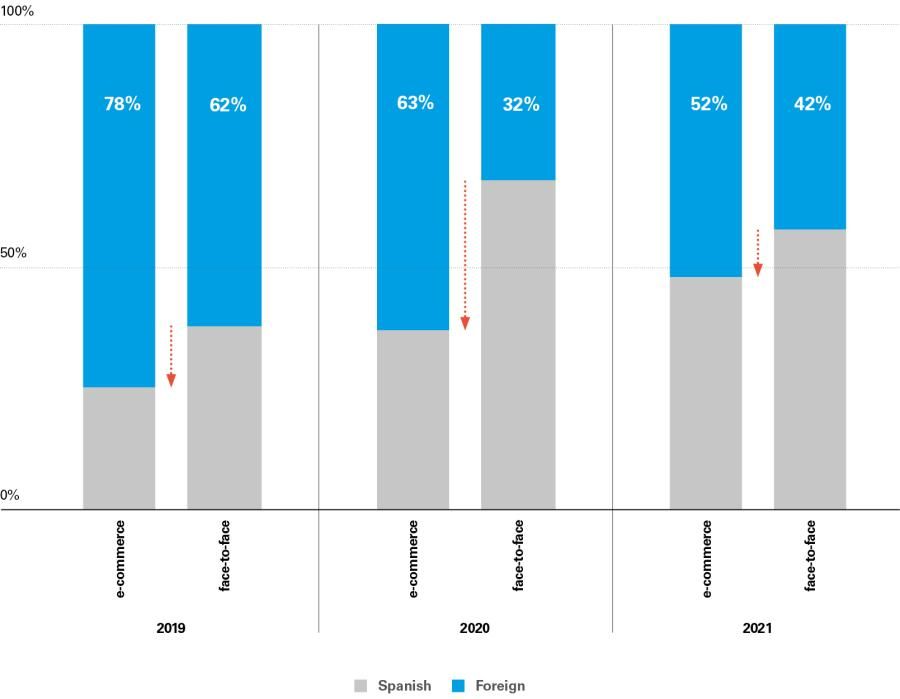

Regarding supply, the greater focus on online sales channels has been a successful formula, offering much more visibility and access to a much larger market for all types of destinations and hotels, regardless of the amount of resources available to invest in marketing. In other words, digital sales channels make it possible for a small hotel in a municipality in Spain that is not particularly tourism-oriented to sell bookings to a tourist on any continent in the world. If we examine CaixaBank POS terminal payments in hotel businesses between 2019 and 2021, we can see that the likelihood of a foreigner making a purchase from a hotel business is substantially higher via the e-commerce channel. This is even the case in 2020, when the volume of foreign tourists in Spain was 79% lower than in 2019, although 63% of foreign tourist expenditure on hotels was carried out via online channels.

Breakdown of payments via CaixaBank POS terminals with accommodation businesses by origin of tourist and sales channel

(% of total expenditure)

Sales of tourism services are already relatively digitalised, confirming the enormous potential of digitalisation to improve competitiveness and productivity. However, according to the CSDI results analysed in this article, there is still a lot of scope for improvement in other areas (B2B relations, investment in technological capital, greater use of data analytics, etc.) which could play a key role in the industry’s future. To progress in digitalising these weak points, it will be necessary for companies in the sector to invest decisively in digitalisation.

by an international tourist was greater via e-commerce sales channels

But not everyone in the tourism industry will be a winner. Traditional sectors with less capacity to digitalise could lose market share, leaving room for those businesses that do develop their digital channels. According to our analysis, the main winners of digitalisation could be: (i) smaller tourism companies, with more potential to improve their efficiency than large companies; (ii) companies offering differentiated services, given that online sales provide a wide range of options for the buyer, and (iii) tourists, who will have access to a larger number of services that are more personalised and more competitively priced.

As noted earlier in this article, digitalisation requires considerable investment. However, the crisis caused by the pandemic has significantly limited the investment capacity of tourism companies. The role played by the European NGEU funds through the Recovery, Transformation and Resilience Plan (PRTR) could therefore be crucial. Spain’s tourism industry appears in the PRTR via the policy of «Modernisation and digitisation of the industrial fabric and SMEs, recovery of tourism and promotion of an entrepreneurial nation Spain», in which component 14 outlines a Plan for the Modernisation and Competitiveness of the Tourism Sector. Despite this, the item budgeted to digitalise the tourism industry within component 14 of the plan is only 337 million euros, a figure that seems very limited given the size of the sector which, in 2019, achieved a tourism GDP of 154 billion euros (investment in digitalisation would represent 0.2% of tourism GDP in 2019).

are limited but could act as a lever to revitalise private investment in digitalisation

The objectives of the PRTR’s Digital Transformation Plan for the tourism industry have focused on developing digital platforms that add value or represent a growth lever for the sector. Consequently, the three main lines of action will be:

- Investment in developing smart destinations to boost Spain’s tourism brands.

- Developing a tourism intelligence system for public authorities and companies in the sector, so that data are collected from the companies and organisations along the entire value chain.

- Investment in innovative projects and initiatives involving digital solutions for the sector (developing applications, collaborative platforms, etc.).

In conclusion, the lines drawn out by the plan are highly appropriate given the weaknesses identified in this article in the tourism industry’s digitalisation. Although we estimate that the extent of the resources allocated in the PRTR for these initiatives is limited, we do expect it will have a leverage effect and revitalise private investment initiatives in digitalisation that were put on hold with the outbreak of COVID-19. In any case, the tourism industry will have to get back on its pre-pandemic track by investing heavily in its transformation, and especially in its digital transformation.

- 14. See «e-commerce: years of progress in just a few months» from our Retail Sector Report 2021 and the Focus «The COVID-19 outbreak boosts remote working» from our June 2020 Monthly Report.