From LIBOR to SOFR

On 30 June 2023, the publication of data on the USD LIBOR, the interest rate at which banks lent US dollars to each other, was ceased. This was not a sudden end, as the relevant authorities had been warning since 2017 of the need to abandon the LIBOR in favour of another benchmark, the SOFR. In this article we explain what these acronyms refer to and which are the differences between them.

What was the LIBOR and why did it stop being published?

LIBOR stands for London InterBank Offered Rate. It was the average interest rate on transactions that a selection of banks carried out with one another on a daily basis, for each currency and maturity term, and it was regulated by the FCA.1 That is, on a specific day, of all the loans denominated in, say, US dollars which banks granted to each other for a one-month term, the average interest rate at which these transactions had been carried out was calculated in order to obtain the 1-month USD LIBOR. This interest rate was of the utmost importance, since the rate on many loans granted to households and non-financial firms was linked to it.

However, following the financial crisis and partly due to the reduced willingness of banks to lend each other liquidity, the number of such transactions sharply declined. From then on, the average was no longer calculated according to the transactions actually carried out; instead it began to be based on the results of a survey in which the banks were asked what interest rate would be applied to such loans.2 This detracted from its representativeness and even led to episodes of bad practices.

Given the importance of the LIBOR, the FCA began working on alternatives to the base interbank interest rate before discontinuing the publication of the LIBOR in January 2022, in the case of the LIBOR denominated in British pounds, Japanese yen and Swiss francs, and in June 2023 for the version denominated in US dollars.3

- 1The United Kingdom’s Financial Conduct Authority.

- 2Andrew Bailey, the current governor of the Bank of England and then CEO of the FCA, explained that for one particular currency and maturity term there were just 15 transactions in all of 2016. See Andrew Bailey’s speech entitled The future of LIBOR, given on 27 July 2017 in Bloomberg, London.

- 3In this article we focus on the case of the US and its new benchmark interest rate, the SOFR, but for the aforementioned countries there are also new alternative rates that have replaced the LIBOR. In the United Kingdom the main benchmark is now the SONIA (Sterling Overnight Index Average); in Switzerland, the SARON (Swiss Average Rate Overnight), and in Japan, the TONA (Tokyo Overnight Average Rate) and the TIBOR (Tokyo InterBank Offered Rate).

What is the SOFR and how does it solve the problems of the LIBOR?

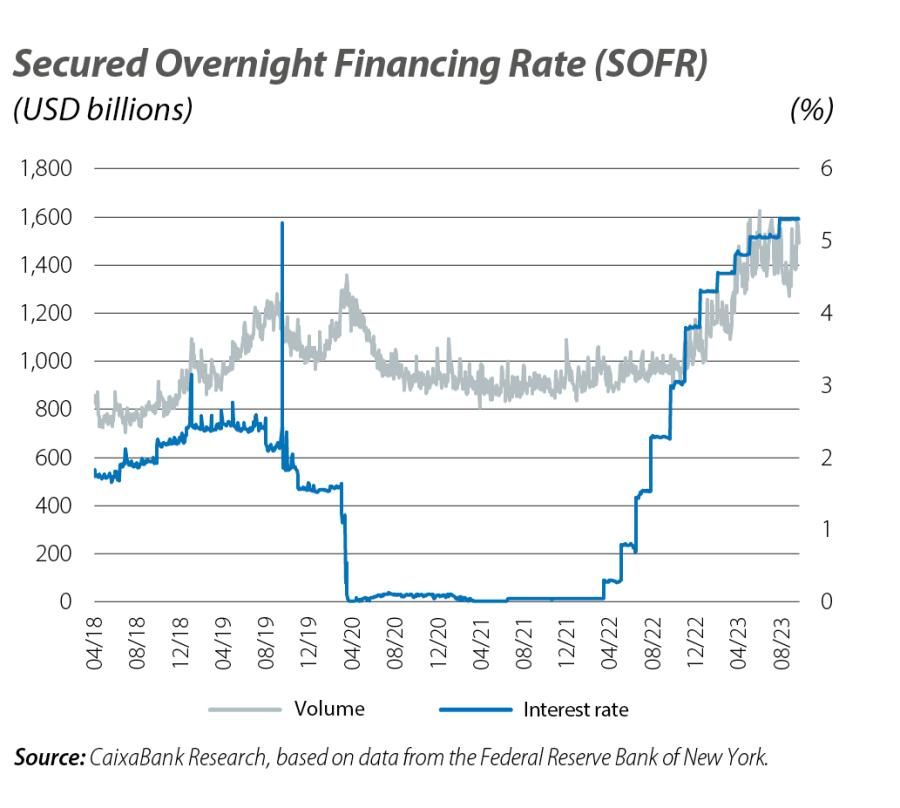

Focusing on the case of the US dollar, the SOFR (Secured Overnight Financing Rate) is an interest rate developed by the US Federal Reserve which has been published since 2018. This interest rate is the result of calculating the weighted average of all one-day loans granted by various financial institutions to each other within the Federal Reserve System. Conceptually, this makes it similar to the LIBOR. However, as we will see later, there are important differences. In fact, since it began to be calculated, the volume of the daily transactions used to calculate the SOFR has exceeded 1 trillion dollars on average, with a minimum value of 0.7 trillion dollars, thus limiting the main problem with the LIBOR: its limited representativeness.4 In addition, the SOFR is published by the New York Federal Reserve based on the transactions actually observed, rather than reported transactions.

- 4This greater representativeness is the result, in part, of including other financial institutions (insurers or fund managers, among others) in addition to the major banks. For further details on these transactions and how the SOFR is calculated, see: https://www.newyorkfed.org/markets/reference-rates/sofr.

Are the LIBOR and the SOFR equivalent?

Conceptually, both are interest rates resulting from observing transactions between financial institutions. However, in the case of the SOFR, the loans that are used to calculate the benchmark are secured by US sovereign debt, while the loans used to calculate the LIBOR have no collateral and are thus unsecured. This means that the level of risk involved in the transactions used to calculate the SOFR is generally lower than in those used for the LIBOR, and the interest rate is therefore slightly lower.

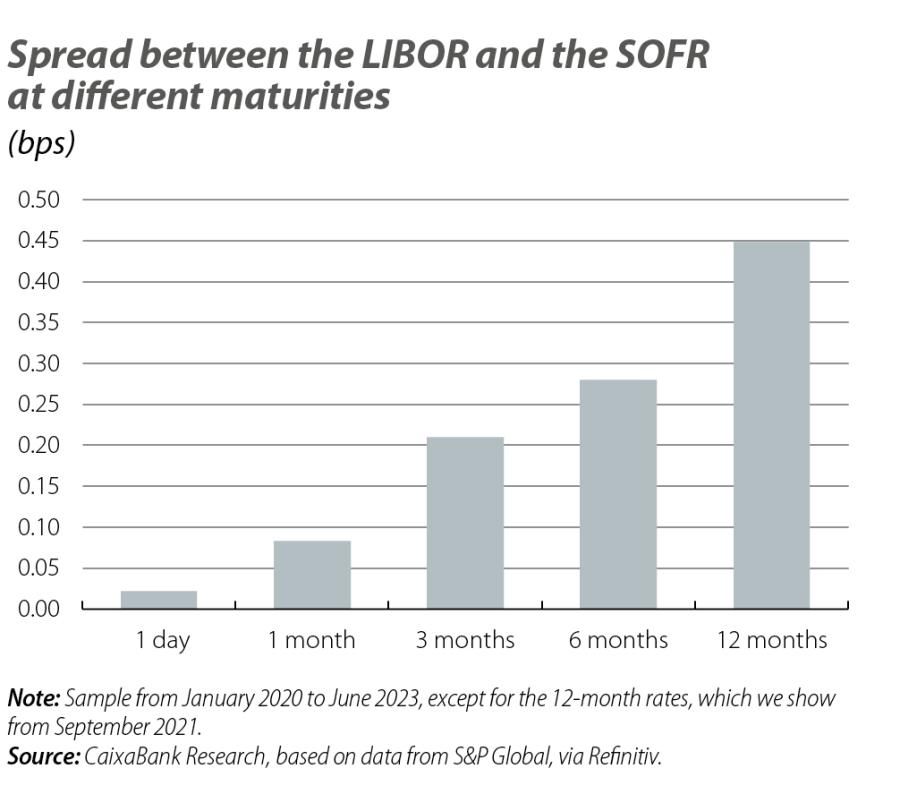

Another major difference is that in the case of the SOFR only the one-day interest rate is published, by definition, whereas the LIBOR was also reported for the interest rates on interbank transactions with terms of 1 week, 1 month and 3, 6 and 12 months. In order to obtain the interest rate at these maturities under the new system, the Chicago Mercantile Exchange (CME) calculates the implicit interest rate using SOFR futures at these maturity terms and publishes them on its website.

However, considering the differences between the LIBOR and the SOFR, the latter offers us reasonable continuity as a metric of interbank interest rates in the US.

What about the Euribor?

These types of interbank benchmarks were revised for all major advanced-economy currencies in order to improve their representativeness, and the Euribor, with its various maturity terms, was no exception. However, unlike the LIBOR, for the Euribor the calculation methods were improved and since 2019 the same indicator has been published but with an improved methodology.5

- 5For further details, see the Focus «Questions and answers about the Euribor» in the MR07/2022.