High volatility in a new geopolitical environment

The start of 2025 has brought a change in the focus of the financial markets, which was consolidated in February. Investors have shifted their attention away from the central banks, which were the main driver of the markets in 2024, towards an environment of high geopolitical risk, with the «Trump effect» as a key catalyst.

Change in investor sentiment

The start of 2025 has brought a change in the focus of the financial markets, which was consolidated in February. Investors have shifted their attention away from the central banks, which were the main driver of the markets in 2024, towards an environment of high geopolitical risk, with the «Trump effect» as a key catalyst. The uncertainty derived from his trade policy and the spending cuts in the federal government, which affected both business and consumer confidence (see the International Economy - Economic Outlook section), began to reinforce the narrative that US economic growth will moderate over the coming quarters and triggered a risk-off movement in the country’s risk assets as risk appetite wavered. In the euro area, the markets are navigating the trade uncertainty amid developments in the war in Ukraine, including a change of stance on the part of the US, a possible negotiation for an

end to the conflict and an intensification of pressure on the euro area to increase defence spending, at the same time

as Germany held elections and entered a new phase of negotiations to form a government. The geopolitical landscape has thus taken centre stage in the financial markets, and the hightened uncertainty has led to a spike in volatility.

The central banks are advancing at different speed

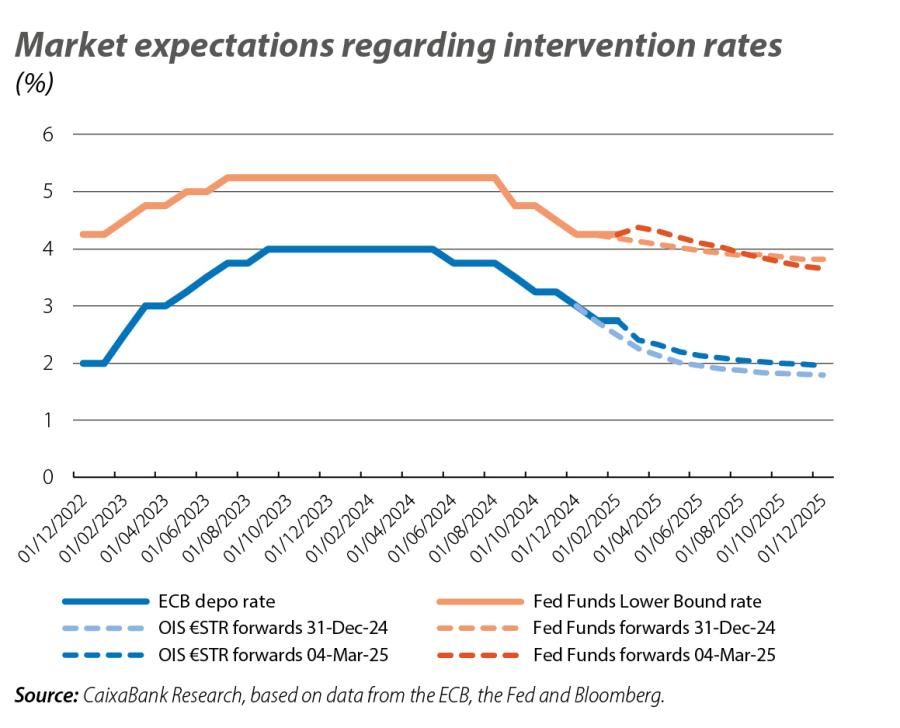

February was a month of limited activity from the central banks. The main meeting was the Bank of England's, which cut its benchmark interest rate to 4.50%, the third 25-bp reduction since August, and the Monetary Policy Committee highlighted the gradual approach planned for future rate cuts. It is this same caution that is guiding the Fed’s strategy, as the minutes of its last meeting in January reveal, in which the FOMC members highlighted the elevated uncertainty and the risk of more persistent inflation. Factors such as possible changes in trade and migration policies were identified as key risks. However, in the last few sessions of the month, the markets have begun to anticipate the likelihood that the Fed will pursue further rate cuts than previously anticipated if activity weakens, as the recent confidence indicators suggest. On the ECB’s side, expectations are still that the depo rate will reach 2% in the summer, which is considered a neutral level and where it are expected to remain throughout the second half of the year.

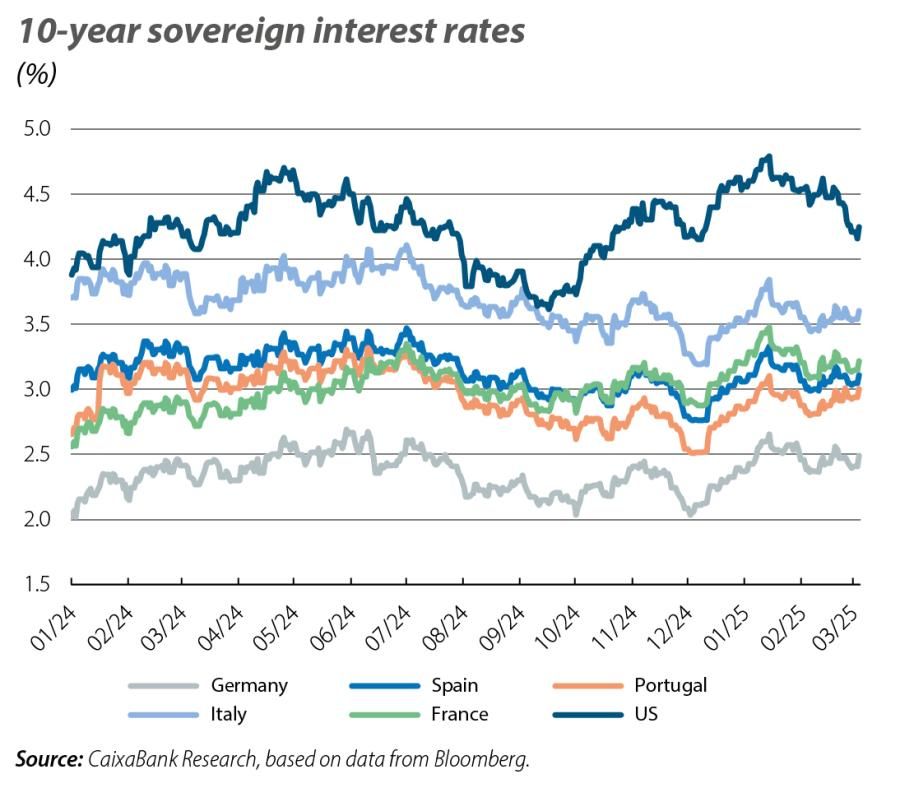

Sovereign interest rates reflect the economic and political uncertainties

In the euro area, on the one hand, expectations of a more dovish ECB and Trump’s delay in imposing tariffs on the EU drove down yields, but on the other hand, the growing pressure to increase defence spending exerted an upward force. Thus, euro area yields experienced round-trip fluctuations in the month, finally ending up with slight declines. In the US, the feeling of risk aversion directed flows towards Treasuries as a safe-haven asset, driving down yields. Declines of up to 30 bps were recorded in the long end of the curve, mostly driven by the fall in real rates (the nominal interest rate on a sovereign bond can be broken down as the sum of the real interest rate plus expected inflation, or break-even inflation). This suggests that the markets are beginning to anticipate an environment of lower growth and higher inflation, in which the future fiscal policies and their effect on the deficit and debt are yet to be clarified.

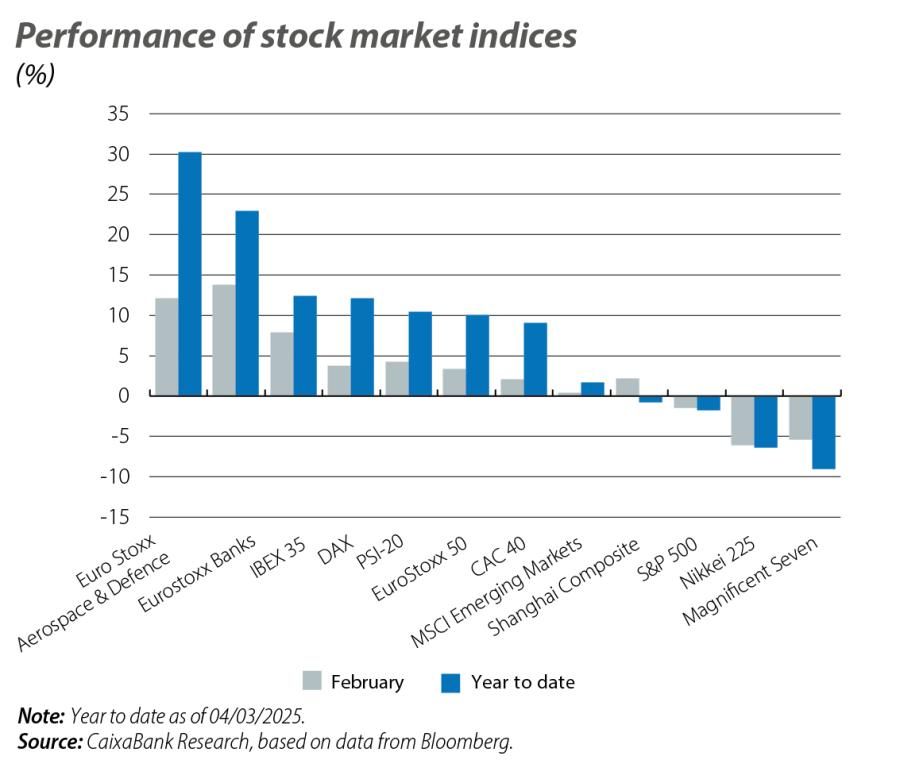

European fixed income emerges as a leader

In line with the risk-off tone of the month, US shares closed February with losses and, at the time of this publication, will have completely erased the gains of the post-election rally. By sector, technology and consumer discretionary (both cyclical in nature) have been the worst performers. In contrast, the main euro area indices have shown a much stronger performance, recording gains of over 10% in the year among the region’s main stock market indices. The biggest driver of the rebound has been the defence sector (+30%), given the new geopolitical context, although the banks (+26%) have also acted as a catalyst following a good earnings season. Moreover, the better performance of European stocks compared to those of the US is occurring in a context of high relative valuations in the US, which makes its markets more vulnerable to negative macroeconomic surprises. In the euro area, meanwhile, where valuations had been depressed relative to those of the US, the margin for gains is greater.

The euro strengthens

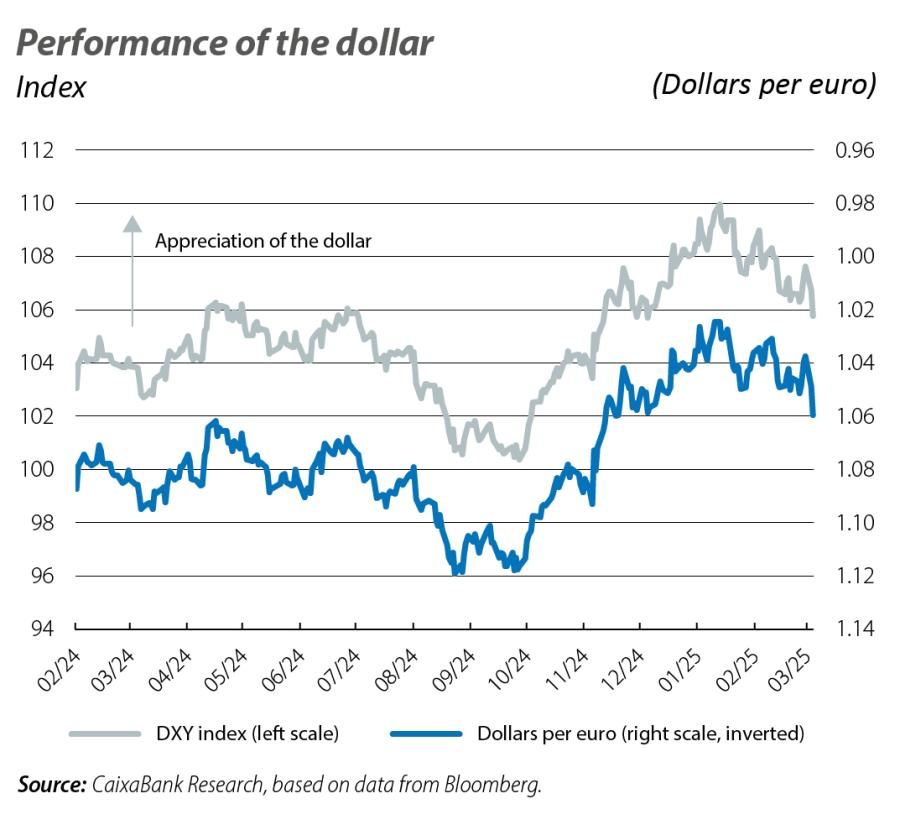

The euro closed the month with gains against the dollar, trading close to 1.06 dollars, up from the 1.03 observed at the beginning of February. The delay in the introduction of tariffs on the EU, a possible deal in Ukraine and a deterioration in the macro outlook in the US have all acted as appreciating forces for the currency. The yen also appreciated against the dollar amid greater expectations that the Bank of Japan will continue to raise interest rates (inflation picked up in January again). In contrast, both the Mexican peso and the Canadian dollar depreciated at the end of the month following President Trump’s confirmation of the reinstatement of the 25% tariffs on imports from both countries.

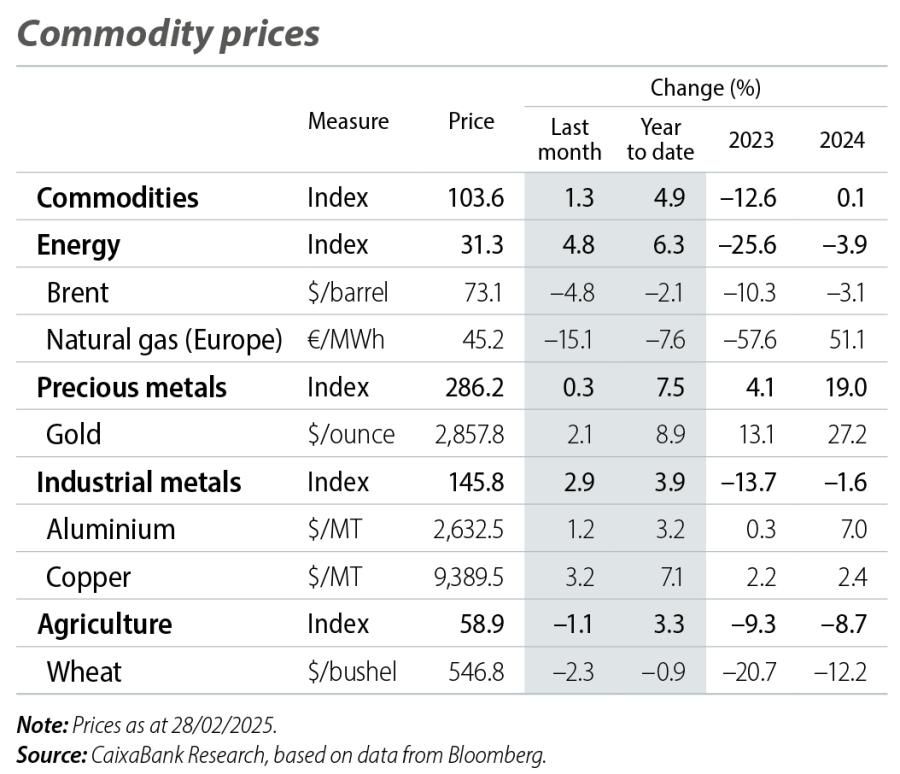

The month of gold

The uncertainty surrounding tariffs has also translated to the commodity markets and has led to a widespread rise in prices, as well as incentivising advance purchases, exerting even more upward pressure. The price of gold, a safe-haven asset per excellence, has surged by almost 10% in the year, and this comes in the wake of the price increases of 2024, reflecting the economic and geopolitical uncertainty. On the other hand, energy has moved in the opposite direction. Gas prices have fallen sharply amid expectations of a resolution of the conflict in Ukraine, as have oil prices in the face of the uncertainty over the slowdown in US demand. In addition, OPEC and its allies confirmed their intention to begin reversing the oil production cuts beginning in April, after more than two years reducing supply, applying downward pressure on prices.