COVID-19 and inflation: a statistically significant impact

In recent years, European inflation has been stubbornly below the ECB’s desired rate, and since 2018 it has been slipping even further away. This weakness has intensified with the COVID-19 crisis. Will this weakness be temporary or permanent?

- The weakness of European inflation has intensified in recent months, reaching negative rates and all-time lows.

- This weakness is largely due to the impact of the COVID-19 crisis. Demand-side factors are largely to blame, but the effect of tax cuts in some countries is also playing an important role.

- Inflation will gain traction with the economic revival, although the scars from the COVID-19 crisis will likely result in a very gradual recovery.

In recent years, European inflation has been stubbornly below the ECB’s desired rate, and since 2018 it has been slipping even further away. This weakness has intensified with the COVID-19 crisis, and core inflation, which reflects underlying price trends, has lost almost 1 pp since January (in October it registered a record low of +0.2%). Will this weakness be temporary or permanent?

The sensitivity of prices to the COVID-19 pandemic

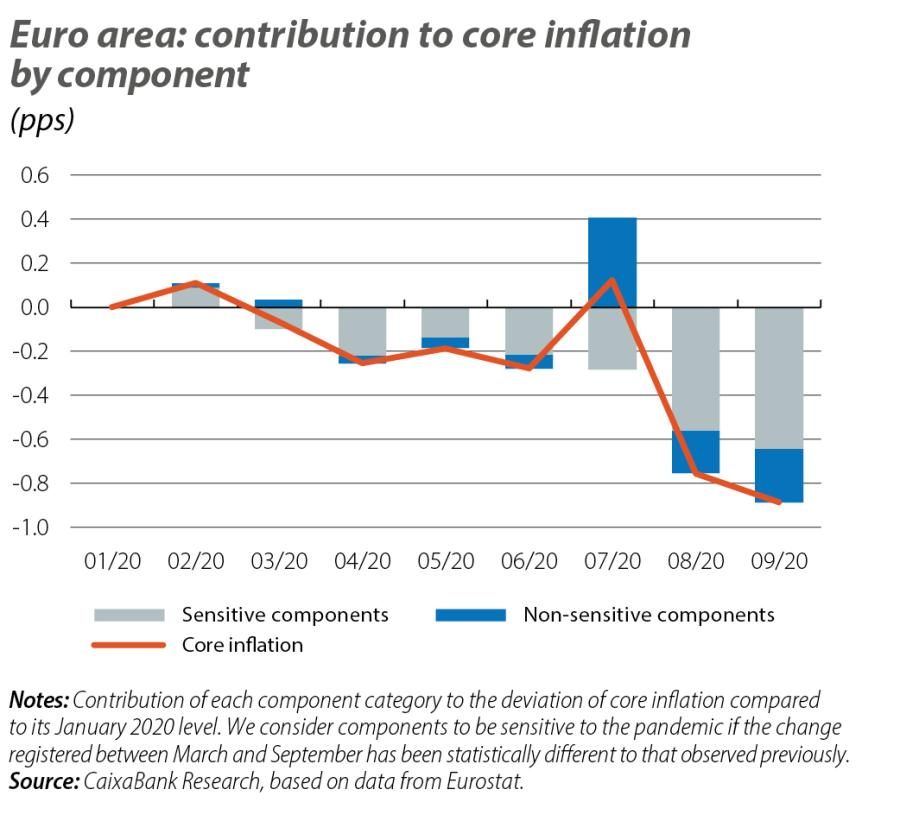

The COVID-19 pandemic can explain a large part of the recent inflation problems. To illustrate this, we will focus on core inflation and, following a methodology similar to that developed by the Federal Reserve Bank of San Francisco,1 we will identify both those components of the set of consumer goods that are «sensitive to COVID-19» and those that have experienced abnormally large price changes since the spring.2 On this basis, 68% of these goods and services in Spain and 51% in the euro area have proven to be sensitive to COVID-19. Some components have shown sensitivity to the pandemic due to them suffering significant price increases, such as in the case of electronic equipment or sporting goods. However, as the first two charts illustrate, most prices sensitive to the pandemic have pushed inflation down and indeed explain the bulk of its weakness in 2020.

- 1See A.H. Shapiro (2020). «Monitoring the inflationary effects of COVID-19». FRBSF Economic Letters.

- 2Specifically, a component \(\;i\) is sensitive to the COVID-19 pandemic if the parameter \(\beta_1\) of the equation \(\pi_{t,i}\;=\;\beta_{0,i}\;+\;\beta_{1,i}\;\ast\;COVID_t\;\;+\;u_{t,i}\) significantly differs from 0. \(\pi_{t,i}\) is the year-on-year change in the price of the component \(i\), \(COVID_t\) is a dummy variable which takes a value of 1 starting from March 2020 and 0 in all other cases, and \(u_{t,i}\) is the error term.

Among the effects of the COVID-19 pandemic, demand-side factors predominate

One of the particularities of the pandemic is that it is affecting prices in very different ways: it has led to a fall in both demand and supply (as well as generating price measurement problems). However, economic intuition helps us to distinguish between one factor and the other: when the shock is on the demand side, prices and quantities tend to move in the same direction, whilst if the shock is related to supply, they move in opposite directions. Thus, the fall in aggregate inflation registered in recent months (in parallel with a fall in economic activity) suggests that the demand-side disinflationary forces have outweighed the reduction in supply. The analysis of the components suggests a similar conclusion. We illustrate this for the case of Spain, where we separate the components between those that have suffered a shock in demand, those that have suffered a shock in supply, and the rest (for which the shock is of an ambiguous nature).3 As the third chart shows, some supply-side forces have driven up prices, but overall they have been moderate and have been offset by the disinflationary pressure of the demand-side shock.

- 3Since we do not have sufficiently detailed data on quantities, we base our illustration on the exercise conducted by Shapiro (2020) for the US, where the necessary level of detail is known. Specifically, if the price of a component moves in the same direction in Spain and the US, we apply the movement of the quantities observed in the US to the case of Spain. Thus, we identify shocks in demand (prices and quantities move in the same direction), in supply (movements in opposite directions) and others (non-significant movements in quantities and/or prices). For instance, in a case where there is no significant change in quantities, there may be a combination of shocks acting in opposite directions. On the other hand, if there are no significant changes in prices but there are in quantities, this would indicate simultaneous shocks in the same direction.

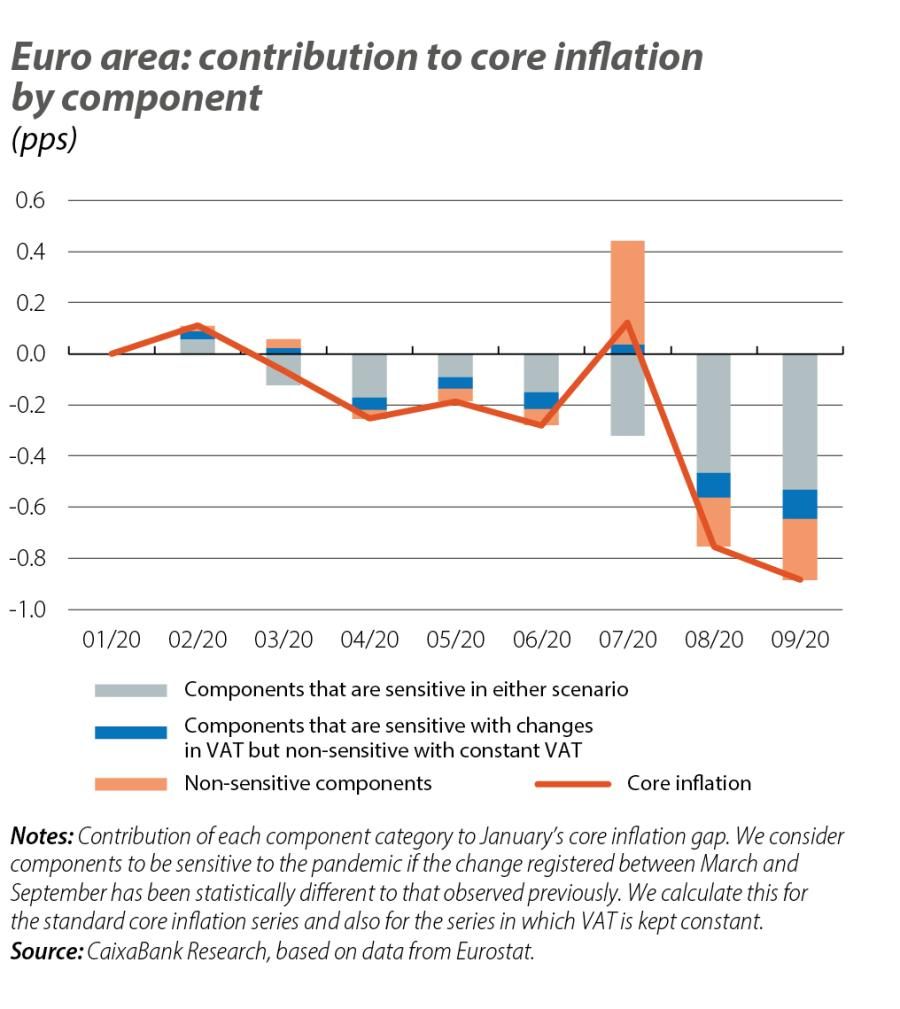

Euro area: VAT also plays a role

Another factor must be added for the euro area as a whole: the VAT reduction. To address the economic crisis caused by the COVID-19 pandemic, some countries such as Germany, Belgium and Austria included a reduction in VAT in their fiscal stimulus packages. In Germany, for instance, the federal government reduced this tax from 19% to 16% for most products, and from 7% to 5% for many others, between July and December 2020. Since a VAT reduction has a direct impact on the purchase price, it could explain some of the fall in inflation. In fact, Eurostat publishes an inflation series in which it maintains taxes constant and which suggests that core inflation in 2020 would have been 0.7 pps higher without the VAT effect.

If the VAT reduction has such a significant impact, it could have tainted our estimates: could it be the case that the pandemic-sensitive components we have identified are only so because of the impact of VAT? This may be partly true, but not in most cases: 65% of the components that we initially identified as being sensitive to the COVID-19 pandemic remain so if we correct for the impact of taxes (the remaining 35% cease to be sensitive).4

- 4Although they remain «sensitive to COVID-19», these components exhibit more moderate price fluctuations after correcting for the effect of the VAT reduction.

Therefore, when the VAT reduction is reversed in the coming months, inflation will bounce back. Nevertheless, the sensitivity of many of its components suggests that, beyond the statistical effect of taxes, inflation will continue to show weakness as long as the pandemic continues to restrict economic activity. It is therefore the economic recovery that will help inflation to return to pre-pandemic levels. That said, faced with the prospect that the revival of economic activity could take a long time to be completed, it appears likely that the ECB will still have work to do over the coming quarters to steer inflation towards its target (below, but close to, 2%).