The Treasury’s funding needs in 2022: within the right range thanks to the support from the ECB

Despite the expected reduction in the deficit to around 5.0% of GDP in 2022, the Treasury’s funding needs will remain high. This leads to the question of whether it could experience difficulties in capturing this funding now that the ECB has announced that it will be reducing its purchases of public debt.

The Treasury’s strategy for 2022, published in early January, states that its planned net issues for this year amount to 75 billion euros and that they will be fully covered by medium- and long-term instruments. This is a similar amount to in 2021. On the other hand, the gross sum of medium- and long-term debt issues, which adds anticipated repayments, will amount to 148 billion euros (12.8% less than in 2021).

The funding requirements for 2022 (excluding bills) will continue to be largely met (more than half) by the ECB. Specifically, the net funding requirements of what the ECB will buy will be lower than in 2018 and 2019, although higher than in 2021 and 2020 (see first chart). In part, this is due to the smaller volume of purchases that the ECB will make this year compared to 2021, which should not surprise us given the gradual process of monetary policy normalisation that will be carried out as the economic recovery is consolidated.1

- 1. The ECB announced that it will make net asset purchases amounting to 480 billion euros in 2022 across the euro area as a whole, less than half of those made in 2021. In this context, it is estimated that the ECB’s net purchases of Spanish public debt will be reduced by 60% compared to 2021, from 126 billion to 50 billion euros. However, the ECB will continue to reinvest assets at maturity.

Another positive element besides the ECB’s support is the diversity of the investor base with holdings of Spanish debt (see second chart). In addition, in 2021 (with data up to October), foreign investors showed their confidence by increasing their holdings of Spanish debt (excluding bills) by 15 billion euros. In this regard, the issuance of the first green government bond in 2021 has made it possible to access new institutional investors.

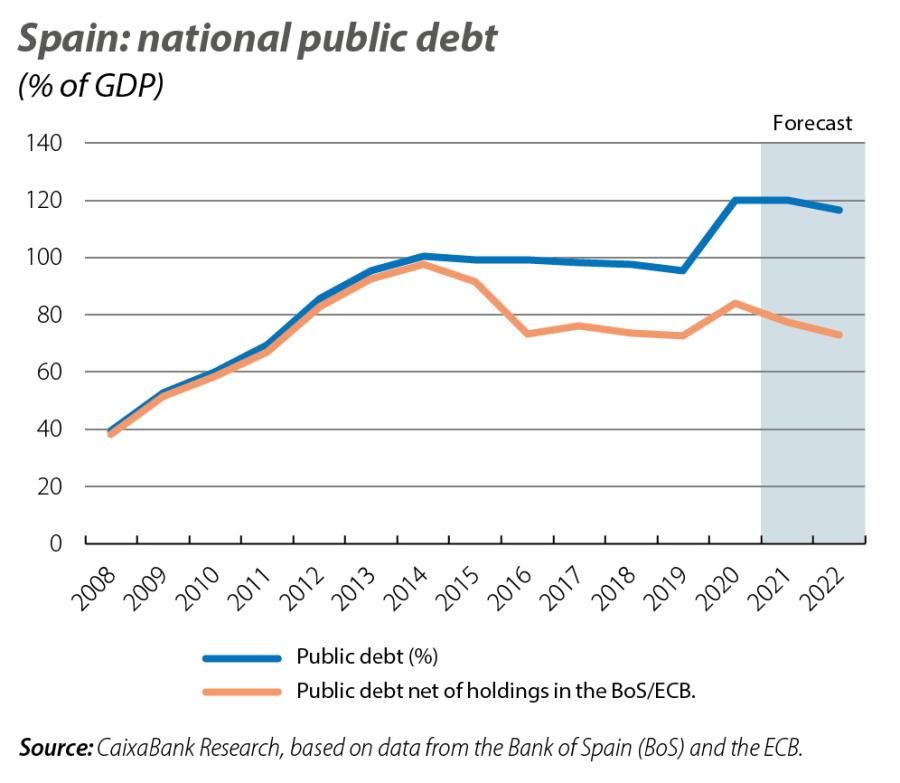

Looking at the total stock of public debt (which we place at around 116% of GDP in 2022), we estimate that the portion in the hands of the ECB will represent 43% of GDP in 2022, leaving the remaining 73% of GDP in the hands of other investors.

There are other key factors beyond the important support from the ECB that help us to understand under what conditions the Treasury will have to meet these funding needs in 2022, such as the abundant liquidity and low financing costs.

It should be noted that in 2021, for the first time in history, the average funding cost of new emissions was negative (–0.04%), with more than 60% of transactions issued at negative rates (including bills, see fourth chart). This reduction has also allowed the average cost of the debt as a whole to continue to fall, bringing it to 1,64%. This is 22 bps lower than in 2020 and marks an all-time low. To anchor these low funding costs, the Treasury has chosen to carry out issues in the longer tranches of the maturity curve, and this has allowed it to increase the average lifespan of Spanish debt, which reached 8 years in 2021 for the first time (7.8 years in 2020). This figure ought to stabilise, or could even increase slightly, in 2022.2

- 2. For 2022, the average lifespan of the stock of debt is expected to stabilise at that level or to increase slightly, settling within the range of 8 to 8.2 years. See the yellow book of the 2022 General State Budgets.

In 2022, the declining trend in the average cost of the debt as a whole is expected to continue, due to interest rates remaining low and because the debt issued years ago that is yet to reach maturity has higher rates. Thanks to the better financing conditions, the general government’s interest burden relative to GDP – one of the main indicators of the sustainability of the debt – stood at 2.1% of GDP in 2021 and is expected to fall below 2.0% in 2022. To put these figures in context, in 2012, for instance, government debt represented 85.7% of GDP but the interest bill stood at 3.0%.

Looking ahead to the medium term, this favourable environment will not last forever, and given the high levels of public debt it will be key to design a fiscal consolidation strategy that is both gradual and sustained over time, as well as being credible in the eyes of international investors.