The rise in commodity prices and its impact on inflation

How is the rise in commodity prices affecting the prices of final consumer goods? What about its impact on developed and emerging countries?

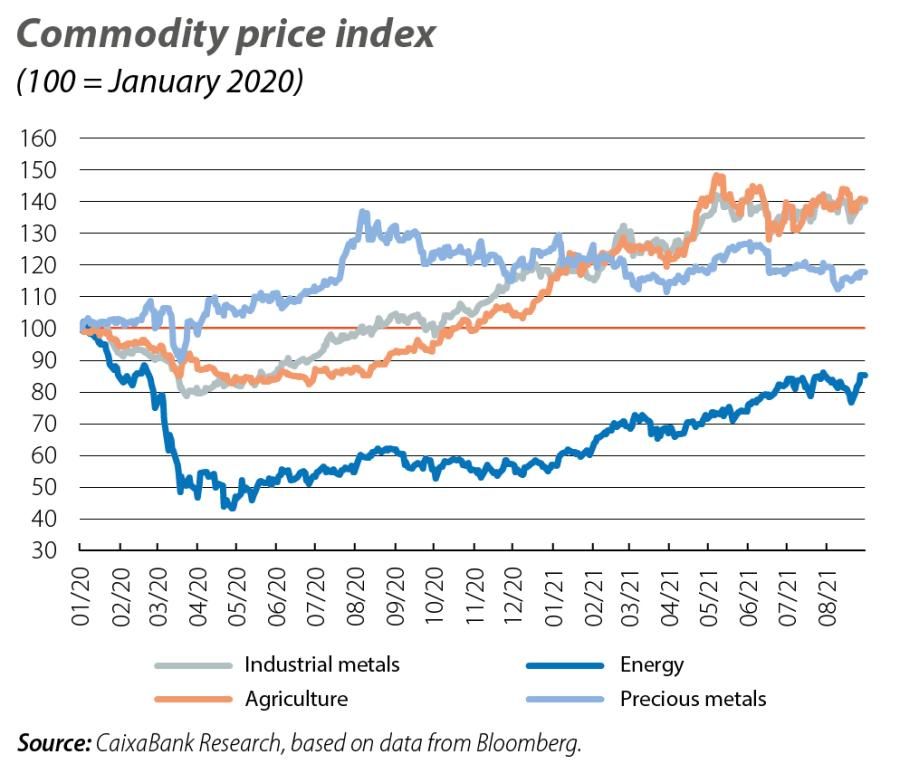

The recovery of the global economy following the shock of the pandemic, in a context of abundant financial liquidity and a highly expansionary fiscal policy in the major developed countries, has favoured rising commodity prices. In the first two quarters of the year, Bloomberg’s general commodity price index rallied more than 20%, largely driven by the rise in energy prices (44.5%), followed by the less pronounced but nevertheless important increase in agricultural goods (20.5%) and industrial metals (17.6%).

A few months ago we analysed the forces behind the rebound in commodity prices.1 The main messages are still valid: the rally is due to a combination of demand-side factors (economic reopening, with a particularly strong revival in industry), supply-side factors (reduction in inventories) and financial elements (increased appetite for risk and depreciation of the dollar). In the current context, in which economic revival co-exists with rising inflationary pressures, we pose ourselves the questions: how are prices of final consumer goods affected by the rise in commodity costs, and what impact does this have on developed and emerging countries?

- 1. See the Focus «Commodities: the resurgence of a market in the midst of the global recession» in the MR02/2021.

In advanced economies, the relative weight of the food and energy components in the consumer price index is usually relatively contained.2 However, movements in energy and food prices are more erratic than in the other components, so they are generally excluded when measuring the underlying trends in prices in these economies. For the same reason, these fluctuations do not tend to have a decisive influence on medium-term inflation expectations, and this is what we have seen in recent months with the modest rise in inflation expectations (see second chart).3 The credibility and communications policy of the monetary authorities of both regions have also played a part by helping to anchor medium-term inflation expectations.

- 2. For example, in the US CPI, energy accounts for 7% of the total, while food represents around 15%. In the euro area, these components have a slightly higher relative weight (10% for energy and 20% for food).

- 3. In addition, much of the aligned movement shown in the chart is due to other factors. For example, since mid-2020, the economic reopening has favoured both a rebound in commodity prices and a recovery in inflation expectations.

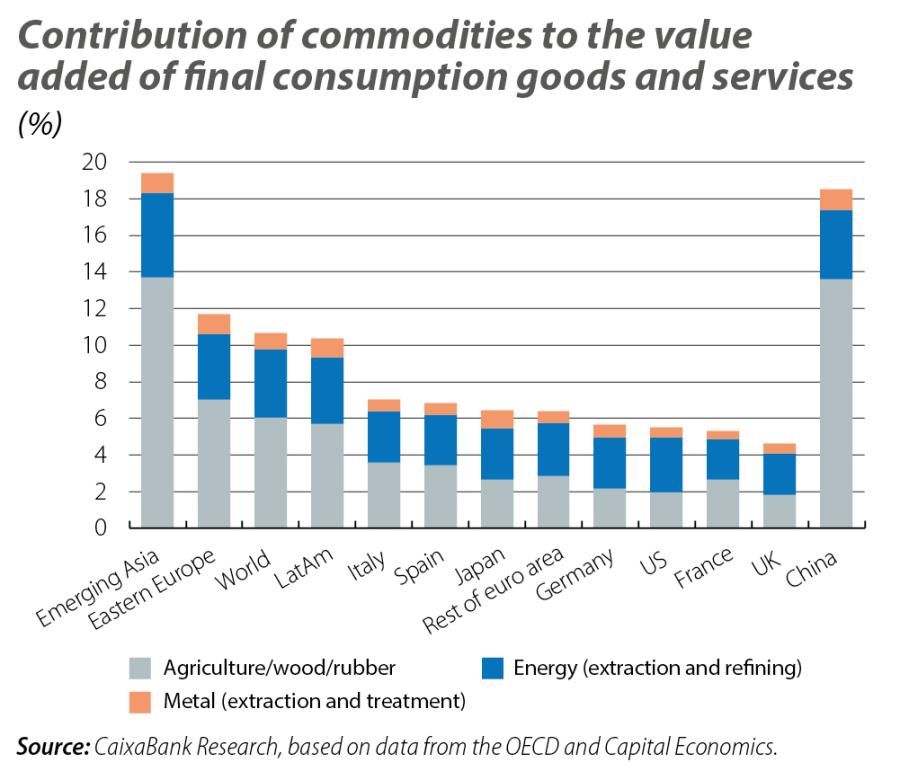

Beyond the direct impact that commodities have on the various components of consumer price indices, it is also important to assess potential indirect effects. As an example, a rise in oil prices not only affects the petrol prices paid directly by consumers but also raises companies’ production costs, which ultimately impacts the final prices of the goods and services that are produced. Thus, it is necessary to take into account how the cost of commodities contributes to the value added of final consumption goods and services. In developed economies, this contribution is low, ranging from 4% to 8% (see third chart), partly because of the prevalence of the services sector in their economic structures. The situation in emerging countries is quite different, as their production and consumption models are more commodity-intensive. We therefore find that emerging Asia, for instance, is more exposed to commodity prices than the euro area or the US.

Moreover, in emerging countries energy and food have a higher relative weight in consumer price indices than in developed economies. Specifically, food accounts for more than 25% of the total index in Brazil and Turkey, while in Russia it accounts for 36% and in India, around 40%. In other words, emerging countries are often more vulnerable to food price rallies, which means that rising food prices affect headline inflation more directly than in developed economies.

The rise in prices of agricultural goods (mainly maize, wheat, soya and livestock) which occurred during Q2 this year was linked to temporary supply barriers (such as droughts, insect plagues and livestock diseases), but it highlighted the sensitivity of many emerging countries to food inflation and the risks that could materialise in the event of a sustained price rally. On the one hand, the rise in inflation, and in particular in the prices of essential goods, deals a heavy blow to consumers’ disposable income in many of these countries (which is already low). In some cases, it can even fuel the risk of social discontent, as happened in the Arab Spring (2010-2012). On the other hand, these economies’ monetary authorities do not enjoy the same credibility among investors as the Fed or the ECB, so they can be forced to act more easily.

The nature of the imbalances observed in the supply of several of these commodities is a response to transitory conditions, so their effect ought to fade over time and should not justify any major shifts in the monetary conditions of many emerging countries. However, since the beginning of the year, one third of emerging countries have inflation rates higher than their central banks’ inflation rate target (such as Turkey, Russia, Brazil, Mexico, Nigeria, Hungary and Poland), and in many cases those high rates are exacerbated by the weakness of their foreign exchange rates. It is in these circumstances that new episodes of surging commodity prices, particularly in agricultural products, could not only trigger rising consumer prices but also a hasty tightening of financial conditions which could hinder the economic recovery.