Global economic activity at a turning point; inflation, we shall see

The set of economic indicators available at the end of Q2 2021 coincide in signalling that, with only a few exceptions, the recovery has turned a corner. The stabilisation of the pandemic, thanks to progress in the vaccination campaigns, is allowing restrictions on movement and social mixing to be lifted, giving a dose of confidence to consumption. As a result, the recovery is gathering momentum and is now spreading to the sectors that had been hardest hit by the crisis. Unless there is an unexpected rise in infections due to the new variants, this trend is expected to consolidate over the coming quarters. The strong rebound in demand, however, has encountered supply-side difficulties, mainly in the form of delays in the supply of industrial sector inputs, but also in the availability of labour in some countries. Our central scenario foresees that these bottlenecks will be gradually resolved without inflicting major harm on the recovery. Nevertheless, the risk that they could persist for longer than expected has increased.

Without undervaluing the good tone of the economic indicators, the focus in recent weeks has once again been on inflation. Indeed, consumer prices have rebounded in most countries, in some cases reaching levels not seen in decades. In addition to the positive base effects, which reflect the year-on-year comparison with the months of «hibernation» in 2020, there have been pressures generated between the rising demand and the supply-side constraints. As we have mentioned, these factors should gradually fade, giving way to a moderation in inflation in the second half of the year and, mostly, in 2022. Nevertheless, the balance of risks is skewed towards a prolongation of the inflationary pressures, and this too is beginning to concern the central banks. In this regard, since the beginning of June, six central banks in emerging markets have announced official rate hikes, while in developed countries there is already talk of the eventual withdrawal of some of the stimulus (see the Financial Markets section).

Another event on the global scene worth highlighting is the agreement reached in early June at the G7 summit on the taxation of large multinationals. Among the main elements discussed is a deal, on the one hand, to set a minimum 15% corporate tax rate and, on the other, a proposal to restructure the way taxes are collected from large multinationals so as to distribute the taxable income base among the various countries in which they operate. The agreement was initially ratified by 130 countries in the OECD in early July. However, a number of obstacles still have to be overcome for it to be implemented (see the Focus «Rebalancing the public finances and corporate tax under the spotlight» in the MR06/2021).

US

The US is the country enduring the most pronounced inflationary pressures. After digesting several rounds of fiscal stimuli, the economy has already reached its pre-pandemic levels in Q2. The pick-up in private spending has spread to the vast majority of economic activities and triggered alarms of overheating in some sectors, such as in the housing market. Business surveys report a shortage of productive factors, which in turn is raising production costs. In this context, inflation has once again been higher than expected: in May it stood at 5% (headline CPI), a level not seen since the run-up to the global financial crisis of 2008. We continue to expect a gradual fall in inflation rates starting from the summer, as the transitory effects fade (base effects, supply constraints affecting suppliers and a labour shortage). Having said that, it is true that the risks of overheating have increased significantly.

As for the labour market, the recovery has been somewhat less robust than that registered in the overall economy, although the rate of job creation did rebound in June (850,000 jobs). Wages, meanwhile, have accelerated, partly due to the difficulties employers are experiencing in filling vacancies. On balance, the number of people in employment is still 5% below the pre-pandemic level, while participation in the labour market remains depressed. We continue to believe that it will still take some time before the labour market shows the «substantial progress» towards full employment that the Fed refers to in its messages (see the Focus «US: (in)complete recovery of the labour market» in this same Monthly Report).

It is precisely the incompleteness of the recovery in the labour market that explains why the Fed has not responded more aggressively to the rebound in inflation. However, at its June meeting the central bank took the first steps towards the eventual withdrawal of some of the monetary stimulus, appearing less complacent about the risk of further inflationary pressures (see the Financial Markets section for further details). On the other hand, in Washington, the Biden administration appears to have secured an agreement in the Senate for an infrastructure plan worth some 1.2 trillion dollars (559 billion in new spending). While still well below Biden’s ambitious infrastructure plan (The American Jobs Plan, which amounted to just over 2 trillion dollars), it nevertheless represents a first step towards the new president implementing his agenda.

EURO AREA

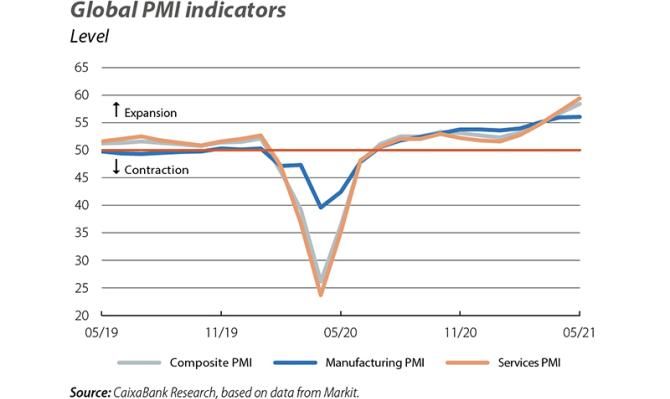

In Europe, after a weak start to the year, the widespread lifting of restrictions is leading to a strong revival in demand, mainly in those sectors that had so far lagged behind in the recovery. In June, business surveys (such as the PMI) reached their highest records in the past 15 years. On the other hand, supply constraints in global chains are already pushing up production costs: in Germany, for example, production prices rose by 7.2% year-on-year in May, the biggest increase in over 20 years. However, unlike in the US, there are few signs that the inflationary pressures have spread to the labour market. Also, consumer price inflation has remained contained (core inflation stood at 0.9% year-on-year in June), at least for the time being. The pick-up in demand and the emergence of bottlenecks could lead to a sharper rise in inflation over the coming months, although we consider these factors to be transitory in nature.

In addition to this cocktail of pent-up demand, the reopening of economies and greater optimism among private agents, yet another factor is arriving on the scene in the form of the approval of new fiscal stimuli, with the distribution of the European Recovery Instrument (Next Generation EU). We expect that the European Council will ratify the recovery plans sent by the various countries, most of which were endorsed in June by the European Commission, and that the first disbursements can be distributed in the summer. As we discuss later on, these will have a greater impact in countries in the south (with Italy and Spain leading the pack) and in the east. The EU transfers and the European Commission’s decision in June to extend the suspension of fiscal rules in 2022 have reinforced the idea that fiscal policy will continue to have a clear easing bias over the coming years.

EMERGING ECONOMIES

Improvements in the pandemic are also evident among emerging economies. A clear example is India, recently at the epicentre of the COVID-19 pandemic, where the number of infections and daily deaths have fallen to their lowest in the last three months. The exception remains Latin America and some regions of Asia (such as Brazil, Colombia and Indonesia), where infections have increased, in some cases reaching all-time highs. However, even in many of these economies, the revival of demand, both internal and external, and the improvement in commodity prices and those of other export goods are causing economic activity to sprout. Our view is that, following a better-than-expected Q1 2021, the recovery will gather pace in the coming months. One risk factor is the shift in monetary policy expectations in advanced economies and the recent strength of the US dollar. The surge in inflation and signs of currency weakness are triggering more decisive responses from central banks.

The latest monthly indicators, generally below expectations, confirm that the Chinese economy has slowed down this quarter as the authorities continue to place more emphasis on stability. That said, the growth outlook for 2021 (around 8.0%) remains well above the official target of 6.0% and leaves room for restrictive financial conditions which aim to continue to support the improvement in the quality of credit. On the other hand, rising commodity prices have driven up production prices (9.0% year-on-year in May), although their impact on consumer prices remains rather moderate (1.3% year-on-year in May).