Quo vadis, globalisation? (part I): the long slowdown

In the last decade, the debate regarding the configuration and consequences of globalisation has gained prominence, with numerous voices advocating a rethink to either limit, reverse or reconfigure it. In this and the following article we analyse the course of these debates and the health of globalisation.

In the last decade, the debate regarding the configuration and consequences of globalisation has gained prominence, with numerous voices advocating a rethink to either limit, reverse or reconfigure it. In this and the following article we analyse the course of these debates and the health of globalisation. To do this, we first analyse the aggregate, longer-term structural trends, before moving on to the more partial supporting evidence from the latest available data. Our goal is to unravel the main dynamics that are occurring in such a complex and, of course, global process.

The gradual slowdown of globalisation...

The clearest hallmark of the economic globalisation that gathered pace in the 1980s was the boom in global trade, but since the global financial crisis this has been showing signs of slowing down, although not stagnating. Focusing on the trade in goods, which is the only form of trade for which we have data in real terms and has been the main protagonist of globalisation to date, it reached its peak with respect to GDP in 2008, after almost 25 years of rapid expansion. It is worth noting that the timing of this slowdown pre-dates the time when the political debate surrounding globalisation gained prominence, suggesting that this slowdown has more complex and diverse causes.

... uneven by country but less so by type of product...

The steady slowdown in trade has not occurred equally across the world’s major economies, as one would expect in a scenario of «radical» deglobalisation (i.e. occurring at the roots). The main culprits of this slowdown among the major exporting economies include the normalisation of China’s growth (an economy now more oriented towards domestic consumption) and a relative stagnation of the US foreign sector. This reduced importance of the foreign sector will also have facilitated a relatively painless trade decoupling for these economies, as explained in the following Focus.

In any case, the foreign sector remains highly important to economies such as the EU and Japan, where exports relative to GDP have continued to increase. However, the recent upturn in this ratio could be distorted by the effects of COVID, both due to the shifts in consumption patterns and because of lower economic growth.

If we look at the trend across different products, on the other hand, the picture is quite different and the slowdown is mainly due to manufactured goods. Having been the driving force of globalisation, in the last decade the growth rates of trade in these goods have been similar to those of world GDP in current prices, meaning its relative weight has stabilised at around 15% of GDP. Fluctuations in the relative weight of commodities, which are reflected in the ratio of exports to GDP in nominal terms but not in real terms, are due to changes in price more than in volume, while exports of services, which could be another growth vector for globalisation in the coming years, continue to gradually gain importance.

... and driven largely by the financial environment

The slowdown in the trade of manufactured goods would be of particular concern for the health of globalisation if it were due to the decoupling of global value chains (GVCs). To evaluate the evolution and length of GVCs we can use a measure that has been proposed by some authors,1 namely the ratio between value added and gross production, which adds the value of all intermediate inputs to gross value added. When companies in a given country specialise and production becomes more diversified and is increasingly relocated offshore, the ratio between gross domestic value added and gross production decreases. This ratio is therefore inversely proportional to the length, or complexity, of GVCs.

- 1See Richard Baldwin (2022). «Globotics and Macroeconomics: Globalisation and Automation of the Service Sector». ECB. Forum on Central Banking 2022.

Indeed, in global aggregate terms, and as is the case with the trade in goods, the expansion of GVCs has already reached a ceiling, having remained virtually stable over the last 10 years. Nevertheless, it is also difficult for now to see a clear and widespread reversal. However, as we will set out in the next article, we are beginning to see concrete signs of fragmentation and relocation to more similar economies.

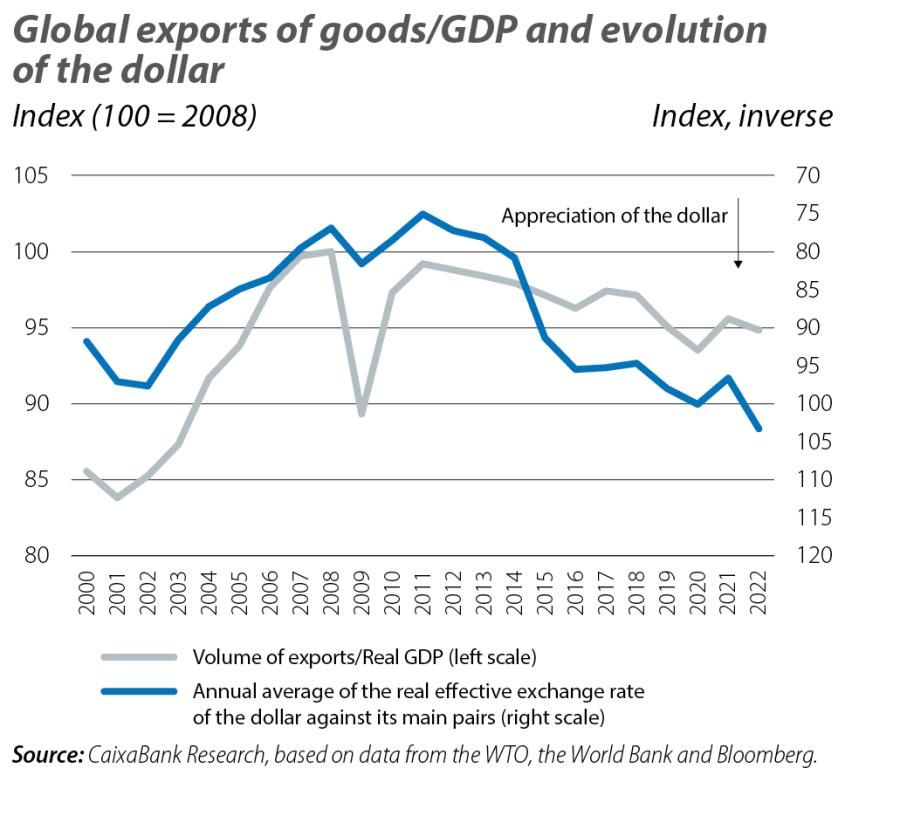

On the other hand, the evolution of the macro-financial environment does appear to be contributing more directly to the slowdown in the trade of manufacturing goods. According to several authors,2 the development of GVCs facilitated production methods – such as the famous «just in time» method – which demanded very high current investment and financing. Relocating a production chain offshore involves a higher level of working capital for any company (i.e. inventories in transit at any given time between the different stages of the process) and, therefore, a higher financing cost, and this increases with each new phase of offshoring.3 Therefore, the development of GVCs was heavily dependant on global financial conditions and, therefore, on the strength of the US dollar (USD).

Thus, even if a strong dollar could make US imports cheaper, it would also hinder the financing of complex production and exporting processes in the rest of the world, weighing down global trade. In fact, since the early 2000s, the strength of the USD and the buoyancy of the global trade in goods have shown a close correlation.

This correlation is also observed with exports from the major Asian economies, so the recent appreciation of the dollar against their currencies, resulting from higher interest rate expectations in the US given the resilience of the country’s economy, could pose an impediment for international trade in the remainder of the year.

Trade globalisation has been showing signs of slowing down for 15 years now, although this is not the case across all countries. In addition, for now and in aggregate terms, it does not seem to be due to a shortening of GVCs. One possible explanation for this trend, raised by some of the studies cited, is that the widespread offshoring of manufacturing to Asia or to countries of the former Soviet bloc, driven by the arbitration offered by skilled and cheap labour, appears to have been exhausted. This could be due to the economic development of these countries as well as because of the process itself reaching maturity, causing firms to reassess the convenience and profitability of offshoring based on their decades of accumulated experience and depending on the needs of the various parts of the production process. On the other hand, financial conditions, which were able to support and encourage the process at the beginning of the century, have not been so favourable in recent years, and even less so after the latest cycle of interest rate hikes since 2022.