Tense calm and spring recovery in the financial markets

The financial markets broadly stabilised during the month of April, as investors' radar moved away from the financial turmoil of March to focus on the growth and inflation outlook, with the publication of GDP data for Q1 2023 and the corporate earnings season.

The financial markets broadly stabilised during the month of April, as investors' radar moved away from the financial turmoil of March to focus on the growth and inflation outlook, with the publication of GDP data for Q1 2023 and the corporate earnings season. Thus, the main risk assets experienced a first fortnight of tense calm and modest recovery, before zigzagging in the latter weeks in the face of signs of persistence of the inflationary pressures, fears about a global economic slowdown and doubts surrounding the financial stability of some US regional banks, which have been the subject of the crisis, culminating with the collapse of First Republic Bank over the May bank holiday weekend. The main central banks, meanwhile, stressed the need to keep rates higher for longer, albeit reiterating that this was dependent on the evolution of the economic data. In this environment, the international stock markets closed the month with mixed results and sovereign yields rose slightly, while the US dollar depreciated against the major currencies. The volatility metrics reflect this stabilisation throughout April, albeit with ups and downs and still fluctuating at historically high levels.

This tense calm paved the way for the central banks to forge ahead with their monetary tightening process, albeit at different speeds and with growing divergences regarding the possible next steps. On the hawkish side, the ECB and the Swedish Riksbank once again stood out, with official rate hikes of 25 and 50 bps, respectively, and the clear intention to continue raising them over the coming months. Meanwhile, the US Federal Reserve raised rates by 25 bps to the 5.00%-5.25% range, although signalling it could pause the process in the coming months if inflation continues to fall and the labour market continues to normalise. A similar strategy could be adopted by the Bank of England, which, in the face of an upside surprise in the inflation and wage data, is likely to announce one final rate hike at its May meeting. In contrast, central banks in some emerging markets (such as South Korea) have opted to pause the rate hikes, in some cases even setting the stage for the start of rate reductions (in Hungary, for example). Finally, at its first meeting with Kazuo Ueda as governor, the Bank of Japan kept the dovish bias of its monetary policy intact and announced an 18-month review to recalibrate its policy framework.

In this environment, the implicit rates in money markets rose relative to March and returned to the levels anticipated at the beginning of the year. Thus, at the end of April investors were anticipating that the ECB will bring the depo rate up to 3.75% in September and will begin a gradual process of rate reductions in 2024. For the Federal Reserve, in contrast, the markets assess that the peak has already been reached and that rate cuts totalling 75 bps will be approved between now and the end of the year. Although significant, this is a smaller reduction than that expected in mid-March. These revisions have been reflected in a widespread rise in sovereign rates, although the main benchmarks are still below the levels prevailing prior to the Silicon Valley Bank collapse. The main sovereign yield curves also continue to show a negative slope between the short sections (2 years) and longer sections (10 years). In the US, short-term Treasury bills have rebounded sharply over fears of a possible default if an agreement is not reached in Congress to raise the debt ceiling.

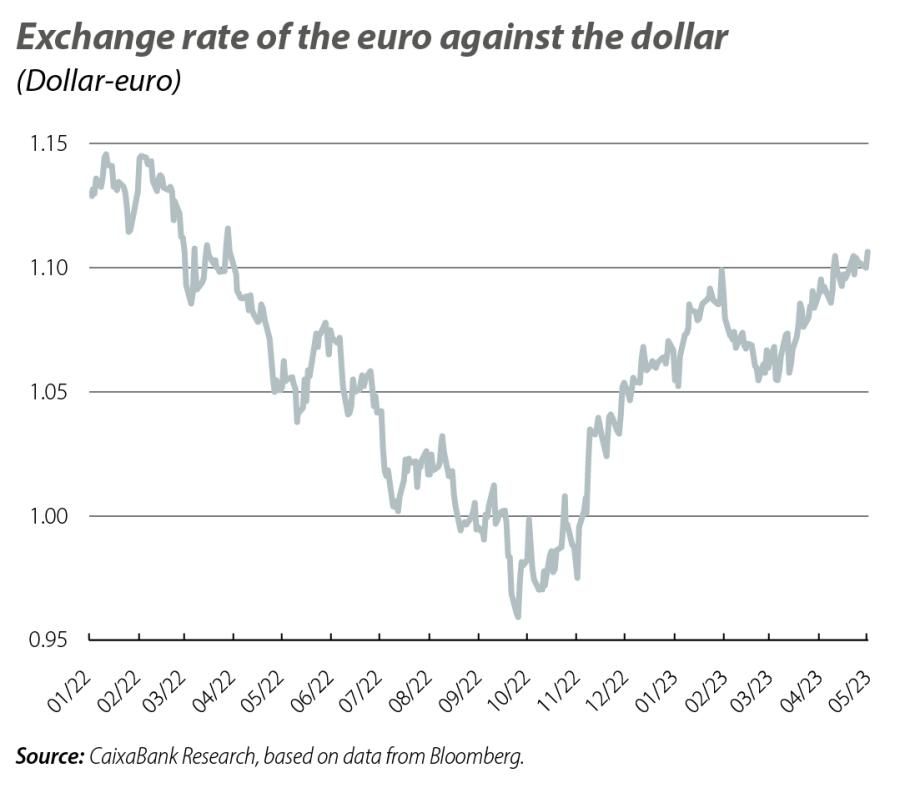

The nervousness around the US debt ceiling, combined with the view that the cycle of official rate hikes has already culminated in the country and that in the euro area, in contrast, still has some way to go, have provided support to the euro exchange rate. The single currency closed April at its highest rate against the dollar for a year, surpassing the 1.10 threshold. The euro has also found support in the improving outlook for the European economy this year, as well as in the perception of the relative strength of the euro area’s banking sector, which has managed to navigate the recent periods of financial turmoil without too many surprises.

Meanwhile, international stock markets enjoyed a significant recovery in the opening weeks of the month (1.8% in the Euro Stoxx 50 and 0.7% in the S&P 500 between the end of March and mid-April), before resuming a negative trend in the closing sessions of the month. By sector, the banking sector was one of the poorest performing, especially in the US, closing April close to year-to-date lows. In Europe, on the other hand, banking stocks closed April with gains, although the sector remains around 10% below the level of the beginning of March. At the other end of the spectrum, the technology sector performed particularly well, spurred on by a good earnings season in Q1 among the big US tech companies and by the furor over technologies associated with artificial intelligence. In emerging markets, stock markets closed April in the red, particularly the Asian indices. Back in March, meanwhile, net foreign capital flows to emerging countries fell by 52% versus the previous month (to 9.4 billion dollars), according to the Institute of International Finance.

Like other assets, fears of an economic recession held back the rise in energy prices throughout April. This was the case for the price of a barrel of Brent, which began the month with a sharp rally following the decision taken by OPEC and its partners to cut supply by just over a million barrels per day, before later ceding ground in light of a potential weakening of global demand. European natural gas prices (Dutch TTF) continued to fall, reaching below €40/MWh (a 21-month low), thanks to the high level of reserves, the growing flow of liquefied natural gas imports and the moderation in demand. In this regard, in its effort to reduce supply costs, the EU launched the first round of joint gas purchases by Member States. In addition, agricultural prices experienced significant volatility due to the worsening of the drought in several producing regions, with sugar prices experiencing a sharp rally in excess of 50% year-on-year as a result of production delays.