Inflation and Omicron in investors’ spotlight

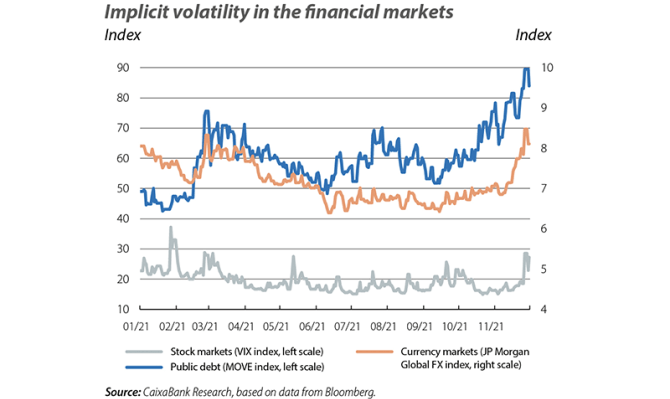

Signs of stress in inflationary pressures and the possible implications for monetary policy were once again the dominant issues in the markets. The credibility of the central banks’ narrative regarding the transitory nature of the inflation rally was dented by the persistence of the bottlenecks, the high energy prices, and the signs that these pressures are spreading to other components of the CPI. Meanwhile, the discovery of the new COVID variant, Omicron, raised fears among investors about the impact it could have on economic growth, given the risk of it leading to new restrictions and exacerbating the distortions in supply. Not surprisingly, in this context volatility has increased somewhat more markedly among fixed-income assets and currencies. In the case of equities, the uncertainty triggered by the Omicron variant led to substantial declines in the stock markets at the end of the month.

In the US, inflation expectations and sovereign debt yields resumed an upward trend, following the higher-than-expected CPI figure for October and the strength of the labour market. However, this pattern was interrupted in the final sessions of the month by the shock generated by Omicron and investors’ resulting flight to safety. Thus, the 10-year Treasury closed the month of November with an 11-bp fall, bringing it to 1.44%. Another important factor as we approach the end of the year will be the approval (or suspension) of a new debt ceiling before 15 December. In the money markets, it is assumed that the Fed will respond with two official rate hikes in 2022 following the completion of the tapering process, which is due to reach its conclusion by the middle of the year according to the plan set out at the November meeting. Our forecasts also foresee two rate hikes in 2022. Meanwhile, US President Joe Biden announced that Jerome Powell will remain at the head of the Fed for a second term.

The speeches given by the members of the Governing Council confirmed a firm position on their view of the price rally as being transitory, while official rate hikes in 2022 are ruled out. In contrast, the markets are assuming that the first increase in depo rates (10 bps) will occur between the end of that year and the beginning of 2023. At the December meeting, the ECB is likely to prolong the TLTROs with less favourable conditions than the current ones and to announce that the end of the PEPP next March could be partially offset by higher purchases under the APP. The ECB’s firmness on the transitory nature of inflation on the one hand, coupled with the deterioration in the health emergency on the other, has been reflected in a considerable weakening of the euro against the dollar. Sovereign bond yields have also registered widespread declines.

The strength of the dollar and investors’ expectations of a more aggressive withdrawal of the stimulus by the Fed has added to the pressure on many emerging-country central banks to approve a new round of official rate hikes. However, these measures were not enough to prevent their currencies from depreciating, a trend which continues to exert upward pressure on their respective inflation rates. Thus, according to the Institute of International Finance, net portfolio flows to emerging economies moderated in October to 24.9 billion dollars (compared to 31.8 billion in September). However, Turkey remains the major exception. Its central bank lowered the official rate by 100 bps for the third consecutive month, weakening the lira to historic lows.

After showing signs of stabilisation in October, the price of natural gas resumed its upward trend and closed the month with a 42% rise (based on the Dutch TTF). The major factors driving this pattern included, on the one hand, the German authorities’ decision to temporarily suspend certification of the Russian Nord Stream 2 gas pipeline and, on the other, the lack of a significant increase in supply to Europe by Russia’s Gazprom. In the oil market, the price of a barrel of Brent behaved erratically, driven by fears of how the Omicron variant might impact demand over the coming months, as well as by the possibility of OPEC revising its rate of supply at its December meeting. This triggered the price to drop to 70 dollars at the end of November, a level not seen since August.

The market shock which began on Black Friday, with the news of Omicron, was enough to undo the gains registered during the month in the international stock markets following the positive Q3 corporate earnings campaigns on both sides of the Atlantic. In fact, for the third consecutive quarter, corporate earnings among companies of the S&P 500 exceeded the analyst consensus forecasts. On balance, the main stock market indices closed the month with marked declines, of 1% in the case of the S&P 500 and of around 4% both in Europe (–8% for the Ibex 35) and in emerging markets. For the time being, caution has taken precedence among investors, who are waiting for new information to weigh up the risk that Omicron could pose for their earnings forecasts.